FINRA’s proposed rule change SR-FINRA-2026-001 is one of the most consequential updates to outside business activity (OBA) and private securities transaction (PST) regulation in years.

If adopted, it would consolidate FINRA Rules 3270 (OBAs) and 3280 (PSTs) into a new Rule 3290, shifting the compliance burden away from low-risk outside activities and toward the activities that regulators believe create the most investor harm.

And yes, this proposal is being positioned as “streamlining,” but firms should be very clear: the rule is not a deregulation. It’s a re-targeting.

What Is FINRA SR-FINRA-2026-001?

SR-FINRA-2026-001 is a proposed rule filing submitted by FINRA to the SEC to modernize how broker-dealers regulate:

- Outside Business Activities (OBAs)

- Private Securities Transactions (PSTs)

The proposed rule creates a single consolidated framework under FINRA Rule 3290, focused on investment-related activities and intentionally excludes “white noise” activities that create documentation and supervision burdens but little investor risk.

The Big Shift: “Investment-Related” Becomes the Trigger

Under the proposal, registered persons must provide prior written notice for any proposed outside activity that is investment-related.

FINRA’s definition of “investment-related” is broad and includes activity involving financial assets such as:

- Securities

- Cryptoassets (even if not technically securities, such as bitcoin)

- Commodities

- Derivatives

- Currencies / FX

- Banking products

- Real estate-related investments

- Insurance products

It also includes roles such as:

- Investment adviser

- Portfolio manager

- Finder / capital introducer

- Sponsor or GP-type roles

- Participation in personal investments where the rep has a beneficial interest

Translation: If money moves, investors are involved, or the public could interpret it as “financial,” FINRA wants it captured.

The Rule’s Core Structure: Selling Compensation vs. No Selling Compensation

The proposed Rule 3290 treats activities differently depending on whether the registered person receives selling compensation.

1) Investment-Related Activity WITH Selling Compensation

If the activity includes selling compensation (commissions, fees, transaction-based compensation, referral compensation, etc.):

Firms must:

- Approve or disapprove in writing

- Supervise the activity

- Maintain records as if it were firm business

- Apply supervisory systems similar to internal firm activity

This is FINRA’s strongest “selling away” control mechanism and it remains intact.

2) Investment-Related Activity WITHOUT Selling Compensation

If there is no selling compensation:

Firms must:

- Acknowledge receipt of the notice

- Conduct a risk assessment

- Decide whether to prohibit or impose conditions

But firms are not required to:

- Supervise the activity ongoing

- Recordkeep as firm business

This is a major change and for many firms, it will reduce operational burden significantly.

What Activities Are Excluded Under the Proposal?

FINRA is explicitly trying to remove “white noise” the kinds of activities that generate endless disclosures but don’t create meaningful investor risk.

Examples of excluded activities include:

- Non-investment side jobs

- Bartending

- Coaching

- Sports officiating

- Farming

- Family transactions with no compensation

- Personal investments in non-securities

- Primary or secondary home transactions

- Activities performed through affiliated entities

- Including affiliated BD/IA structures

The Most Notable Change: Unaffiliated RIA Activity Gets a “Lighter Touch”

One of the most controversial and significant components of SR-FINRA-2026-001 is how it treats registered reps who also operate an unaffiliated Registered Investment Adviser (RIA).

Under the proposed rule:

- The rep must provide notice

- The firm must assess risk

- The firm may impose conditions or prohibitions

But the firm is not required to:

- Supervise the RIA activity

- Recordkeep the RIA activity

FINRA’s logic: RIAs are already regulated under the Investment Advisers Act and/or state regimes, so duplicative broker-dealer supervision may not be necessary.

However, this is where many firms will see increased risk, especially around:

- Customer confusion

- Brand affiliation assumptions

- Referrals

- “Selling away” migration

- Privacy and data handling

- Liability optics when something goes wrong

The U4 Problem: The Proposal Does NOT Change Form U4 Reporting

Here’s where many firms will get tripped up:

The proposal does not amend Form U4 disclosure requirements which remain broader than Rule 3290.

Meaning:

Even if an activity is excluded from Rule 3290 (because it’s not investment-related), it may still be:

- U4 reportable

- Required under firm internal policies

- Subject to regulator scrutiny during exams

FINRA has stated it plans to coordinate with the SEC and NASAA to align definitions and potentially issue guidance but until that happens, firms may need to maintain dual tracking.

What Firms Should Do Now: Practical Implementation Guidance

1) Continue Centralized Submission of ALL OBAs

The safest approach remains:

Require registered persons to submit all outside activities through the firm’s internal process even if the activity is not investment-related.

Why?

- Reduces rep misclassification

- Creates a clean audit trail

- Protects the firm during exams

- Ensures U4 reporting stays consistent

2) Have Compliance Determine What Counts as “Investment-Related”

Firms should not rely on reps to decide what qualifies as investment-related.

Instead:

- Reps submit everything

- Compliance determines applicability

- Supervisory requirements are applied consistently

This will matter most for:

- Crypto-related activities

- Real estate syndication

- “Consulting” roles that include capital raising

- Referral arrangements

3) For Reps With Their Own RIA: Build Conditions and Guardrails

Even though the proposed rule relaxes supervision requirements, firms should strongly consider:

- Written conditions (no client overlap, no referrals, etc.)

- Required disclosures to avoid perceived affiliation

- Annual attestations

- Spot checks for conflicts

- Data privacy controls

- Clear client communications

This is especially critical because “no supervision required” does not equal “no liability risk.”

FINRA’s Estimated Savings: $14–$28 Million Annually

FINRA estimates firms and registered persons could save approximately $14 million to $28 million per year through reduced administrative burdens.

But firms should remember:

Savings are real

but so is the risk of misinterpretation, weak implementation, and exam findings.

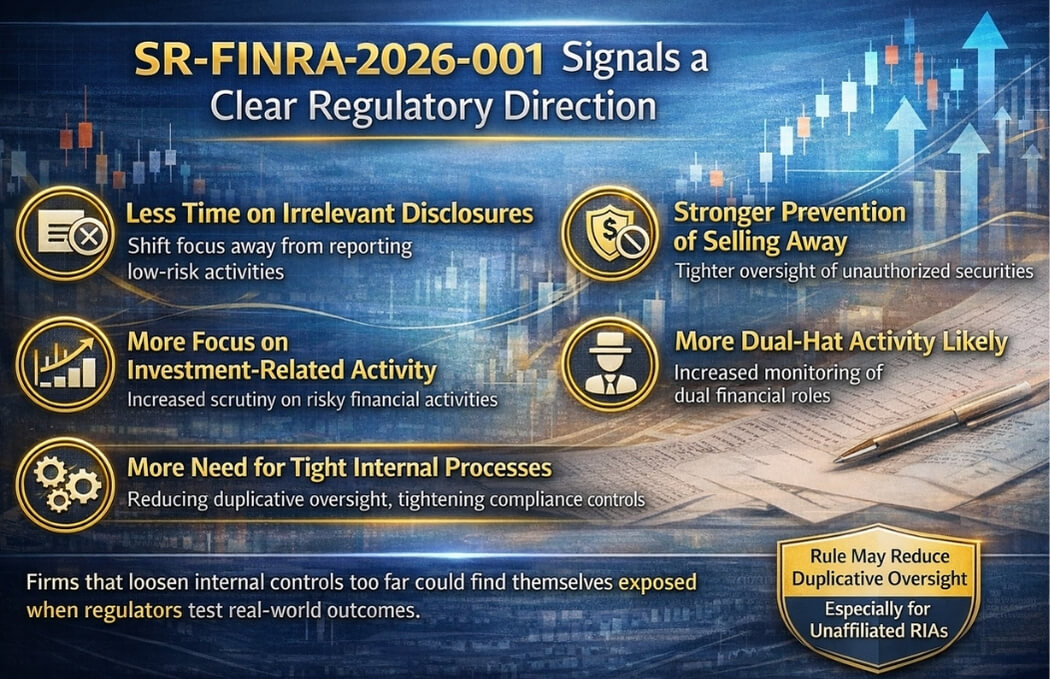

Final Takeaway: Streamlining Is Not the Same as Lower Risk

SR-FINRA-2026-001 signals a clear regulatory direction:

- Less time on irrelevant disclosures

- More focus on investment-related activity

- Stronger prevention of selling away

- More dual-hat activity likely

- More need for tight internal processes

The rule may reduce duplicative oversight especially for unaffiliated RIAs but firms that loosen internal controls too far could find themselves exposed when regulators test real-world outcomes.

Need Help Building Your Rule 3290 Process?

MCG Consulting helps firms design practical, exam-ready workflows for:

- Rule 3290 notice + risk assessment processes

- OBA/PST decision trees

- RIA dual-hat guardrails

- WSP updates

- Supervision models and documentation

Reach out: info@mcgcomply.com